Liar Loans Are Back – And They Could Be Hiding in Your Loan Book

Does your customer base include high-risk customers who have falsified their income to get their loan?

You bet it does.

Two separate pieces of Australian market research recently published on this topic have reinforced the fact that liar loans are alive and kicking in the market. A shockingly high ratio of applicants are continuing to admit to salary deception on their financial applications, as highlighted in a survey concluding in August 2024.

More worrying is that, according to the research, this problem is getting worse—not better.

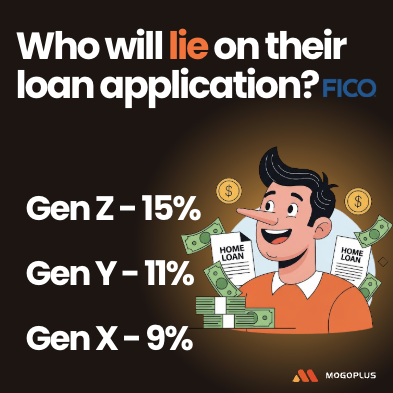

The Rise of Financial Misrepresentation Among Younger Borrowers

FICO found that the emerging Gen Z cohort of younger borrowers (your future target customers?) are significantly more likely to falsify income and create fake documents for income and expenses than their predecessors. This aligns with data from Finder, which discovered that:

- 1 in 3 borrowers have lied on a financial application

- A staggering 52% of Gen Z and younger generations think it’s acceptable to do so

- And 15% of Gen Z admitted to inflating their income specifically on loan or credit applications

These figures were echoed in The Adviser’s recent coverage of the issue, highlighting growing concerns among lenders and brokers. The misrepresentation tactics range from inflating self-employment income and bonuses to omitting debts or fabricating employment altogether.

Why Are People Lying?

The answer is simple: because it’s easy.

With many lenders still relying on self-declared income—especially from ‘new to bank’ applicants—or outdated manual payslip checks, the loan origination process remains wide open to abuse. In fact, FICO’s senior consultant Corey Smith points out that many borrowers don’t even realise this behaviour could be classified as application fraud, which undermines trust in the financial ecosystem, emphasizing the importance of effective analytics to identify and mitigate risks.

Combine that with cost-of-living pressures, housing affordability concerns, and social media-driven expectations, and it’s not hard to see why falsifying income is tempting for younger borrowers.

How Big Is the Problem?

Let’s look at the numbers again:

- 10% of Australians overall have admitted to lying on a financial application with ANZ.

- 53% of Gen Z say lying on loan applications is “normal” or “acceptable in some situations”

- Only 12% of over-65s agree

Many lenders have no reliable mechanism to verify stated income—especially from gig economy workers, freelancers, or the self-employed. As the Australian credit sector enters a new cycle of lower interest rates and rising loan application volumes, this issue is only set to worsen.

Banks loosen stress tests for borrowers refinancing

As the economic landscape shifts, many banks are beginning to relax the stress tests applied to borrowers seeking to refinance their home loan repayments.

This change is particularly relevant in the current climate, where rising interest rates have made it increasingly difficult for homeowners to manage their mortgage repayments. By loosening these requirements, banks are allowing borrowers with lower credit scores or higher debt-to-income ratios a better chance at refinancing, thus enabling them to escape the potential financial pitfalls associated with high- interest loans. However, this strategy raises concerns about the long-term implications, as it may inadvertently encourage borrowers to take on more risk than they can handle.

With many homeowners struggling to keep up with their mortgage repayments, the decision to ease stress tests could lead to a rise in liar loans. This situation is especially concerning since some borrowers might be tempted to misrepresent their financial status on loan applications to qualify for refinancing. Lenders, as Sean Warren highlights, must remain vigilant as they navigate this delicate balance between providing relief to struggling borrowers and ensuring that they do not inadvertently contribute to a resurgence of liar loans. The stakes are high, and the repercussions of these decisions will be felt throughout the financial ecosystem.

The Solution: Data-Led Income Verification

Fortunately, there’s a simple and scalable solution in the market today.

Shifting to a data-led origination model can eliminate liar loans with one simple change. Utilising a transaction data focused solution that has been designed specifically for accurately verifying a variety of income sources not only solves the Liar Loan issue, it also provides automated, accurate and validated insights to gain a richer picture of your new customer.

Put simply, the data doesn’t lie

These solutions can also aggregate data at an application level so various income streams in multi employer and multi applicant scenarios can be captured and combined . This means quicker time to decision, better customer experience and big savings on manual workloads and operational costs.

Data security aspects are also covered with clear messaging and consent based sharing so the customer is always in control.

At MOGOPLUS, we provide a powerful, proven solution to this problem that gives the lender:

- Granular insights: Intelligent categorisation of income across primary, secondary, and recurring sources

- Configurable outputs: Recency, reliability, and regularity of income clearly measured and benchmarked

- Fast automation: No more slow, manual processing of payslips or relying on customer honesty

- Fraud detection and risk reduction: Identify red flags and inconsistencies early in the process

These tools are already in use by leading digital-first lenders across Australia, in all credit products from home loans to personal credit. And no—this doesn’t need to wait for Open Banking to take over the world. Our solution works today and is fully Open Banking-compatible for tomorrow.

A global issue

The issue of liar loans is not confined to Australia; it is a global concern affecting financial ecosystems worldwide. As housing markets fluctuate and property prices soar, instances of financial misrepresentation, including false documents, are becoming increasingly prevalent across various countries. In markets like Canada, for instance, falsified financial documents and income misrepresentation have emerged as significant drivers of mortgage fraud. In fact, Equifax Canada’s analysis revealed that 30.2% of mortgage fraud cases in late 2024 were attributed to falsified financials, indicating a worrying trend that demands attention from financial institutions and regulators alike.

Similarly, in the United States, the property market has witnessed a rise in liar loans as borrowers attempt to secure financing amidst escalating house prices and interest rates. This situation has created an environment ripe for unethical behavior, with borrowers and brokers alike overstating income or misrepresenting assets to qualify for larger loans. The consequences of such actions are severe, often resulting in borrowers facing foreclosure or crippling debt when they can no longer meet their mortgage obligations.

As the global economy continues to grapple with these challenges, it is imperative for financial institutions to implement robust verification processes to combat the rise of liar loans.

The implications of these issues extend beyond individual borrowers; they threaten the stability of the entire financial system. When financial institutions do not adequately verify the information provided by borrowers, they expose themselves to significant risks. The resulting wave of defaults and foreclosures can lead to broader economic instability, mirroring the events of the 2007-2008 financial crisis. It is crucial for lenders worldwide to adopt stricter verification standards and invest in technology that enables them to detect fraudulent applications early in the process, safeguarding their portfolios and maintaining trust in the financial system.

Why It Matters Now

As Finder’s Graham Cooke warns:

“Falsifying income can result in more than just a denied loan. It can damage credit, hinder future borrowing, and potentially lead to legal prosecution.”

That’s not just a borrower problem—it’s a lender problem too, if your portfolio is carrying hidden exposure to liar loans.

At MOGOPLUS, we’ve been working with Australian transactional data in credit decisioning for over a decade. Our experience, focus on data enrichment and intelligent insights, and our deep industry understanding make us the ideal partner for lenders looking to stay one step ahead of financial misrepresentation.

Are more repossessions on the horizon?

As the economic pressures mount and interest rates rise, there is growing concern among experts that the number of home repossessions could increase significantly. Data from various financial institutions indicates that many borrowers are already struggling to keep up with their mortgage repayments, and as rates continue to rise, this situation may worsen.

The Reserve Bank’s influence, along with the combination of rising living costs, increased interest rates, and the potential for additional financial stress has created an environment where more borrowers may find themselves unable to meet their obligations.

This data starkly highlights the risks facing homeowners and suggests that financial institutions may need to prepare for an uptick in repossessions in the coming months. The consequences of these repossessions extend beyond individual borrowers; they can destabilize the housing market, leading to decreased property values and increased economic uncertainty.

As lenders grapple with these challenges, it is essential that they adopt responsible lending practices and remain vigilant in monitoring borrower performance to mitigate potential losses.

In summary, as the landscape shifts and borrowers face mounting pressure, the possibility of increased repossessions looms on the horizon. Financial institutions must take proactive measures to support their customers while safeguarding their own interests.

By implementing more stringent verification processes and offering tailored solutions to struggling borrowers, lenders can help mitigate the risks associated with this precarious situation.

Want to see how easy it is to eliminate liar loans from your portfolio?

Reach out to request a free trial or demonstration.

Our solutions can be easily trialled and tested via our Google Marketplace instance. You can see results in minutes without the need for a heavy integration or API connection. We offer a free 30 day trial so you can see for yourself.

Let’s talk about how we can help you move from risk to resilience in your lending strategy.