The Gig Economy Lending Trap: Why Your Current Income Verification Is Failing Australia’s Fastest-Growing Borrower Segment

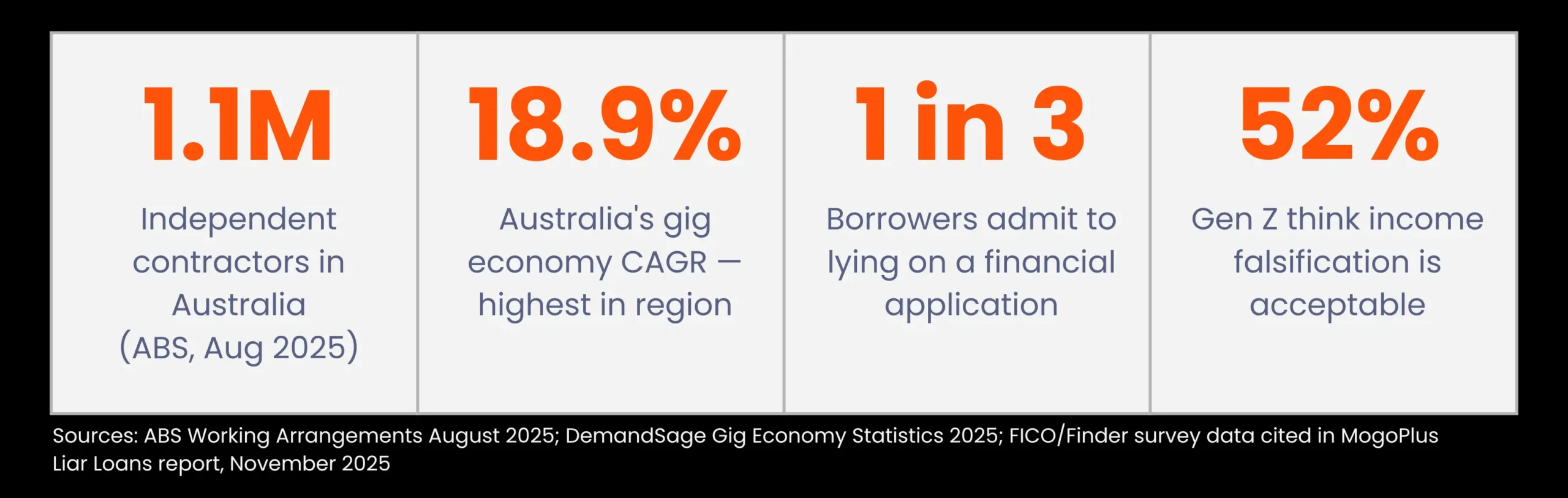

More than 1.1 million Australians now work as independent contractors (7.6% of the entire workforce)

Add in freelancers, sole traders, multi-employer workers, and platform workers, and the true figure of non-traditionally employed Australians seeking credit is significantly larger.

But to most lending systems, they’re invisible – or worse, they’re a risk.

This creates challenges for your current income verification process – without a long term fix you’ll see your loan book quality and growth plummet.

Income Verification Problem #1: Valid customers get rejected because of old school income verification logic

The first challenge for lenders is one of exclusion: potentially qualified borrowers are being declined because their income doesn’t fit the payslip model.

Income Verification Problem #2 – It’s easy to lie, and get away with it

The second challenge for lenders right now is fraud – and it’s more widespread than most lenders want to acknowledge.

The Cause: A Credit System Built for a Workforce That No Longer Exists

Australia’s credit assessment infrastructure was built around one assumption: that borrowers are employees. They receive a regular salary, deposited fortnightly by a single employer, evidenced by a payslip. That payslip becomes the primary proof of income.

For the growing segment of Australian workers who don’t fit this model, the consequences are significant.

The ABS reports that in August 2025 there were 1.1 million independent contractors in Australia with Construction (21%), Administrative and Support Services (22%), and Other Services (14%) leading by industry concentration.

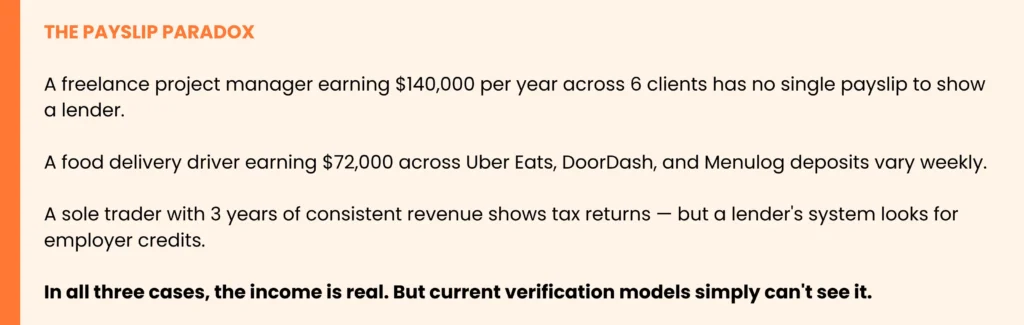

These workers earn income from multiple sources, at variable intervals, from different payers.

Their financial health is real. Their payslip is non-existent.

What the Data Says About Gig Worker Loan Rejection

The mismatch between gig worker income reality and lender verification capability is quantifiable.

Research on the sector consistently finds that non-traditional earners face structural disadvantage in credit access:

- 41% of gig workers face specific hurdles to raise money or loans because of their non-traditional work status (DemandSage, 2025)

- Gig workers, who receive income per task or project, don’t generate the documentation that credit systems require

- Income inconsistency, cited by 28% of gig workers as a financial stability challenge, makes lenders nervous even when average annual income is equivalent to or exceeds that of a salaried borrower

- Payment delays are common in the sector, creating gaps in bank transaction patterns that manual reviewers often misread as income instability

The Liar Loan Problem: Your Current Tools Can’t Detect What They Can’t Measure

There is a darker dimension to the gig economy income verification challenge – and it goes beyond the honest borrower who simply can’t prove their income in the format a lender requires.

It concerns the borrower who knows the system is weak, and exploits it.

Liar loans – applications where borrowers misrepresent their income, employment, or financial position – are back, they are growing, and they are concentrated precisely in the population segment where income is hardest to verify: gig workers, freelancers, and self-employed borrowers.

The Data Is Alarming

A survey cited in MogoPlus’s own Liar Loans research (November 2025), drawing on FICO and Finder data, found:

- 1 in 3 Australian borrowers admit to having lied on a financial application

- 52% of Gen Z and younger believe falsifying income is acceptable

- 15% of Gen Z admit to inflating their income on a loan or credit application

The problem is structural, not incidental.

Fortiro‘s April 2025 analysis of Australian lending fraud patterns found that falsified income represented 14.4% of all fraud cases examined..

Critically, Fortiro’s research found that bank statement templates are now available for free download online, and that documents can be manipulated in under a minute using tools that require no technical skill.

This is no longer sophisticated fraud. It is accessible to any motivated borrower.

The Gig Economy Intersection: Why This Group Is The Highest Risk

The overlap between gig workers and liar loan risk is not coincidental. It is structural.

Gig workers and self-employed borrowers are the population segment where:

- Income is hardest to verify through traditional documentation

- Stated income is most likely to diverge from actual income

- Manual reviewers have the least basis for comparison

The MogoPlus Liar Loans analysis (November 2025) notes directly:

“Many lenders have no reliable mechanism to verify stated income — especially from gig economy workers, freelancers, or the self-employed. As the Australian credit sector enters a new cycle of lower interest rates and rising loan application volumes, this issue is only set to worsen.”

Why Manual Review and Payslip Checks Won’t Save You

The instinct is to apply more human scrutiny. More review time, more documentation requests, more questions to the borrower. But this approach fails on three counts:

- Speed: A credit analyst spending 45 minutes manually reviewing bank statements cannot keep pace with application volumes at growth-stage lenders.

- Accuracy: AI-generated fake documents are now indistinguishable from genuine ones to a human reviewer. Fortiro found that readily available tools can produce convincing falsifications in under a minute. Human review cannot reliably detect what software has been used to create.

Coverage: Manual review cannot catch fraud patterns that require data processing at scale – staged deposits from multiple accounts, circular transfers, temporary employment boosting, or income timing manipulation around application dates.

The Solution: Accurate Transaction Categorisation Is the Only Reliable Answer

The answer to both problems — gig worker exclusion and liar loan fraud — is the same: move from document-based income verification to accurate and advanced transaction-based income verification.

Bank transaction data doesn’t lie. A borrower can edit a PDF payslip. They cannot retroactively alter 24 months of transaction history from their bank’s own data feed.

When income verification is anchored to actual transaction patterns rather than submitted documents, the fraud surface area collapses.

But the key word is “accurate.” Not all transaction categorisation is equal. The quality of the income picture a lender gets depends entirely on the quality of the categorisation engine interpreting those transactions.

Uncategorised transactions are blind spots. Every payment that can’t be classified – every income stream that doesn’t get tagged, every expense that falls into a miscellaneous bucket – is information your credit decision is being made without.

What Accurate Categorisation Actually Delivers for Gig Worker Lending

When transaction categorisation is genuinely accurate – meaning near-complete classification across the full range of income types that Australian borrowers actually earn – the picture a lender gets is transformationally different:

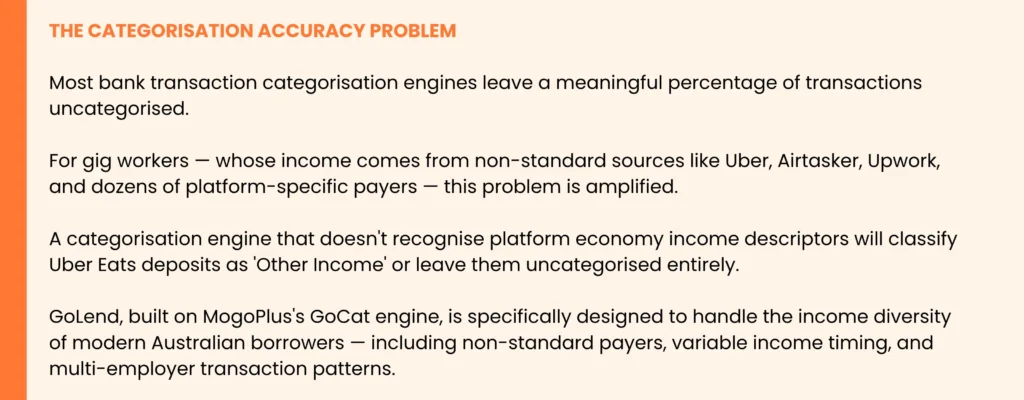

- Gig income visibility: Platform economy payments (Uber, DoorDash, Airtasker, Upwork, Fiverr, etc.) are identified and correctly classified as income — not miscellaneous deposits — allowing a gig worker’s full earning picture to be assessed

- Income pattern analysis: Irregular income from multiple sources can be assessed for average, trend, and reliability rather than requiring a single employer payslip

- Employer verification at transaction level: GoVerify cross-references stated employer against actual transaction history — a borrower claiming $120K salary from a specific employer is verified against actual employer credits in the feed, not just the document they submitted

- Fraud signal detection: Staged deposits, circular transfers, and temporary income boosting around application dates show as transaction anomalies that an accurate categorisation engine can flag — because it classifies the pattern, not just the label

- Multi-applicant and multi-income aggregation: Gig workers often have complex income structures across multiple sources, ABNs, and entities. Accurate categorisation aggregates these into a coherent income and expense profile that a credit analyst can review in seconds, not hours

GoLend: Designed for the Borrower Your Manual Process Can't Assess

MogoPlus’s GoLend product was built specifically to address the challenge of complex income assessment — including the gig, freelance, and non-traditional earner population that represents the fastest-growing segment of the Australian lending market.

Powered by GoCat — MogoPlus’s bank transaction categorisation engine — GoLend delivers:

- Full income classification across primary, secondary, recurring, variable, and platform income sources

- Net Monthly Position tracking across 24 months, showing income trends and volatility rather than a single point-in-time snapshot

- Automated review flags for payday loan dependency, collection agency exposure, gambling patterns, and dishonour fees — the financial stress signals that predict default risk before it becomes visible in a credit bureau file

- Employer verification against transaction history, not submitted documents — eliminating the single largest document fraud vector

- A single API call that replaces the manual bank statement review workflow entirely — from 45 minutes to seconds, with better accuracy and a complete audit trail for NCCP compliance

The result is a lender that can confidently approve gig worker applications that deserving borrowers currently can’t get through — while simultaneously catching the fraudulent applications that current manual processes are missing. That is not a trade-off. It is what accurate categorisation enables.

The Commercial Imperative: Why 2026 Is the Year to Fix This

Three converging forces are making 2026 the year this problem becomes impossible to defer.

1. The Gig Economy Is Only Getting Larger

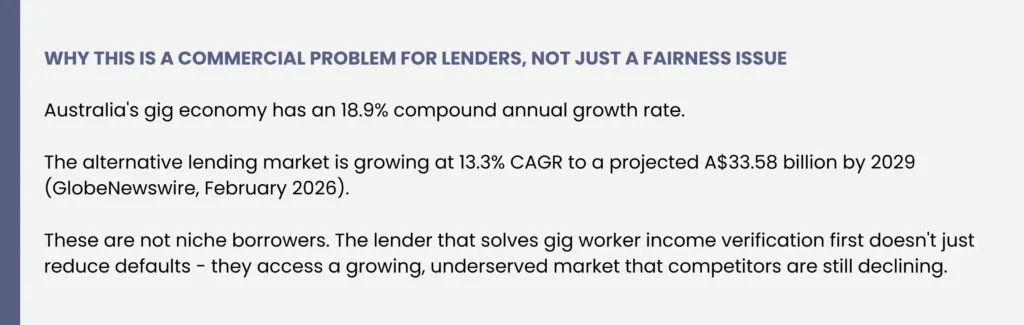

Australia has one of the highest gig economy growth rates in the world at 18.9% CAGR. The ABS August 2025 data shows independent contractors at 7.6% of all employed Australians and rising.

The alternative lending market targeting this segment is projected to reach A$33.58 billion by 2029.

The lender that figures out how to responsibly underwrite gig worker income first does not just solve a problem — they capture a growing market segment that competitors are still declining.

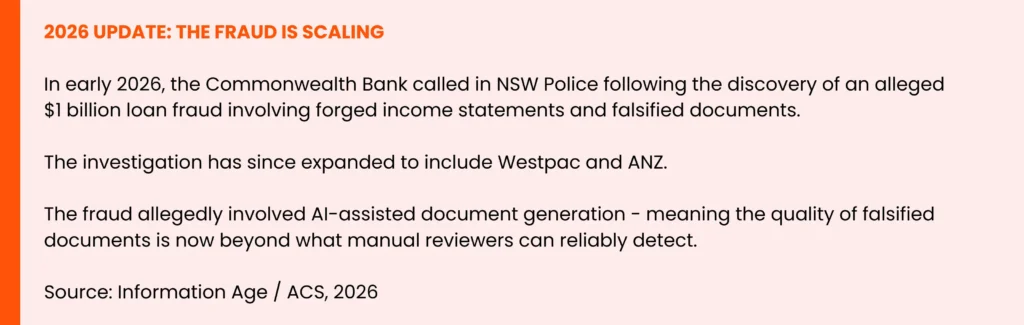

2. Fraud Is Becoming AI-Assisted

The 2026 CBA fraud investigation — involving an alleged $1 billion in loans potentially backed by AI-generated documents — has demonstrated that the arms race between fraud and detection has entered a new phase. Manual document review is no longer a reliable control.

Lenders who do not move to transaction-based verification in 2026 are building their origination process on an assumption of document authenticity that no longer holds.

3. Screen Scraping Is Ending — and the Migration Window Is Now

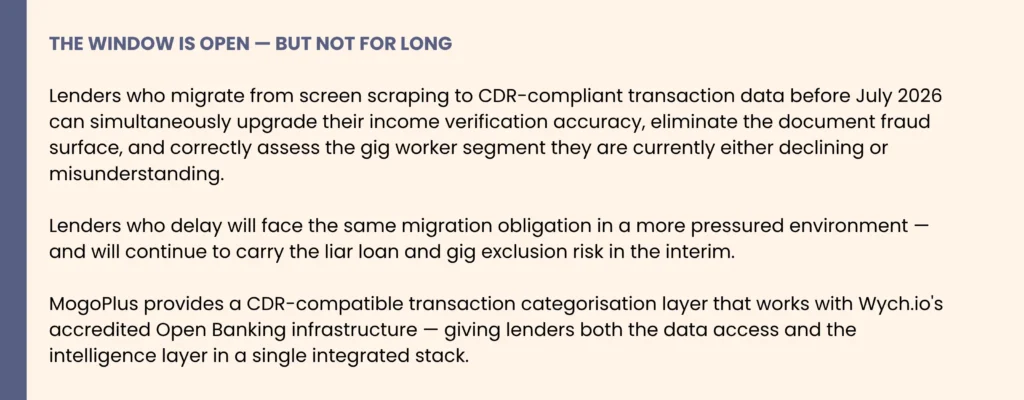

The CDR transition is abolishing screen scraping as a compliant data access method.

Non-bank lenders who currently rely on screen scraping tools for bank statement analysis — whether through illion Bank Statements or other providers — must migrate to CDR-compliant Open Banking data access before July 2026.

That migration is not just a compliance checkbox. It is an opportunity to rebuild the income verification layer on accurate transaction data rather than on the legacy infrastructure that has been the foundation of liar loan vulnerability for the past decade.

Closing Argument: Your Gig Worker Is Not the Risk. Your Categorisation Engine Is.

The gig worker applicant is not the problem. The problem is a credit system that can’t see them accurately — and, as a result, either turns away qualified borrowers or fails to detect the fraudulent ones.

Accurate bank transaction categorisation is the single most effective lever a non-bank lender can pull in 2026 to simultaneously expand its addressable market and reduce its fraud exposure. It does not require a rip-and-replace of your credit engine. It requires an accurate, complete income picture at the point of decision.

MogoPlus has spent over a decade building transaction categorisation specifically for Australian lending. GoLend, GoVerify, GoAssist, and GoCat are used by lenders from Westpac and Arab Bank to Loan Options AI and One Click Life — across the full spectrum of Australian lending, including the borrower types that standard systems can’t handle.

Sources

The following sources were used in the research and preparation of this article:

- Australian Bureau of Statistics — Working Arrangements, August 2025 (abs.gov.au) — Independent contractor figures, 7.6% of employed Australians

- DemandSage — Gig Economy Statistics 2025 (demandsage.com) — Australia 18.9% CAGR; 41% of gig workers face loan access barriers

- GlobeNewswire — Australia Alternative Lending Business Report 2026 (February 2026) — A$33.58 billion projected market by 2029, 13.3% CAGR

- MogoPlus — Liar Loans Are Back and They Could Be Hiding in Your Loan Book (mogoplus.ai, November 2025) — FICO/Finder survey data; 1 in 3 borrowers, 52% Gen Z acceptance rate

- Fortiro — Perspective: Liar Loans, Responsible Lending and Document Fraud (fortiro.com, April 2025) — Falsified income 14.4% of fraud cases; $2.3 trillion mortgage debt exposure; 59% mortgage stress February 2025

- The Adviser — Liar Loans Back in Spotlight (theadviser.com.au, March 2025) — 76% of home loans via broker channel; responsible lending obligations

- Information Age / ACS — AI Heist: CBA Calls Police Over $1B Loan Fraud (ia.acs.org.au, 2026) — AI-assisted document fraud; investigation expanded to Westpac and ANZ

- AUSTRAC — Indicators of Suspicious Activity for Non-Bank Lenders (austrac.gov.au) — Application fraud as primary threat; document falsification indicators

- Jobbers.io — Australia’s New Gig Economy Laws 2024–2025 (October 2025) — Platform worker regulations and deactivation protections

- Frontier Software Australia — The Gig Economy Super Trap (2025) — Superannuation gaps and two-tier workforce analysis

© 2026 MogoPlus Pty Ltd · mogoplus.ai · This article is for informational purposes. All statistics cited to original sources.